Finding funding to start new ventures has long been a difficult task for entrepreneurs, even those with great business ideas, as the traditional fundraising process requires significantly more effort, time, and money. Cryptocurrency fundraising offers an alternative that is best suited for blockchain-related projects. This article will walk through the emergence of various forms of cryptocurrency fundraising, how the fundraising landscape may continue to evolve, and the role financial institutions can play in this area.

The Past Experience of Traditional Fundraising

In the traditional finance textbook, there are two primary sources of funding: debt and equity. Companies can raise debt funding by asking a bank for a loan or issuing corporate bonds. Equity fundraising offers a different set of options. Companies can bootstrap, ask friends and family for small investments, or raise funding from private investors. Startups are typically tech-heavy and require time to generate a positive bottom line, and therefore may require multiple private equity funding rounds over several years before they can access equity funding from public market investors via an Initial Public Offering (IPO).

Following the development of blockchain technology in the late 2000s, Decentralized Applications (dApps), which are web services that use blockchain as a base infrastructure, gained popularity in recent years. The most widely mentioned use for dApps is financial services, referred as Decentralized Finance (Defi). In normal cases, the trustworthiness of the dApp project (also referred to as dApp protocols) will depend heavily on the project roadmap in the white paper, the code presented, and the owners’ background. However, dApp projects do not need to be a registered company and the project owners can be anonymous.

As traditional fundraising can be slow and costly, particularly for entrepreneurs without existing investor networks, an alternative source of funding for dApps has emerged: Cryptocurrency Fundraising (also known as Token Fundraising), where the project owners offer its dApp project’s tokens to interested investors at a relatively discounted price in order to raise funds to run their business. This fundraising method has rapidly gained its popularity due to its benefits relative to traditional fundraising especially for fundraisers, which will be discussed later in this article.

Image source: Maketecheasier – Decentralized Applications (dApps) are digital applications or programs that exist and run on a blockchain or peer-to-peer (P2P) network of computers instead of a single computer. dApps are outside the purview and control of a single authority.

Types of Cryptocurrency Fundraising

There are several ways people categorize the types of token fundraising. One of the easiest ways to understand cryptocurrency fundraising is to break it into Private Placements and Public Offerings. Please note that each country’s regulations might have an effect on the nature of fundraising.

Private Placement

A project owner may decide to conduct a Private Placement in which tokens are offered to a select group of investors prior to a public offering. This is known as a “token presale,” where the startup or project sells tokens while the project is still being developed. The goal of the token presale is to either raise funds for the project’s early development, or for business growth accretion that will eventually lead up to the Initial Coin Offering (ICO) launch. Since token presales are highly risky and investors may lose their entire investment if the project fails to deliver the intended outcome, tokens are usually sold at a huge discount compared to their expected exchange listing price. However, given the cheap price, if the project succeeds, investors will be rewarded with a huge profit. Due to the high risk/high return tradeoff, token presales have gradually become the main event before a new protocol’s public offering as speculators gamble on being rewarded with a satisfying profit.

Public Offerings

There have been three main types of public offerings.

Initial Coin Offering (ICO):

By definition, an ICO refers to the first time when a project raises funds by selling its token to public investors. However, over time the word has taken on another meaning, and now typically refers to any token offering where the project has organized the sale of its tokens by itself. The majority of tokens raised via ICOs are utility tokens. These are tokens that can be used to access and obtain services and products within the protocol. The project may also issue governance tokens in an ICO, which represent the right to vote for the project’s direction. For avoidance of doubt, a token can have both utility and governance features. Unlike an IPO where all fundraising documents are submitted to and evaluated by the Securities and Exchange Commission (SEC) before the company is allowed to issue shares to public investors, in an ICO, the project owner creates a whitepaper which covers all the details of the project. The purpose of the whitepaper is to provide enough details to obtain investor trust, as there is no regulator responsible for verification. One of the most well-known ICO projects was the launch of Ethereum in 2014.

Data source: Coinschedule – According to January 2021 ICO market report, there have been 5,728 ICO projects launched in total. These projects had acquired a market value of $ 27 Billion.

That said, due to the lack of regulation, many projects raised funds but never developed the project promised in the whitepaper. Many of these projects turned out to be scams created by anonymous project owners who ran away with investors’ money, which caused ICOs to lose popularity. Consequently, the undesirable image became one of the major downfalls of this method, along with the need to conduct its own marketing expense to raise funding awareness into investors’ ears. In Thailand, government regulators have stepped in to mitigate some of the trust issues in the ICO market, but two other token fundraising options have also arisen as an alternative to ICOs: IEO and IDO.

Initial Exchange Offering (IEO):

IEO is an improved version of ICO created to address the problems found in the ICO market. An IEO is an ICO where the projects are thoroughly screened and analyzed before tokens are sold on a cryptocurrency exchange. The exchange is responsible for evaluating the credibility of the project, and therefore will need to thoroughly verify the token issuers in order to maintain the credibility and trustworthiness of the exchange. As a result, cryptocurrency exchanges can prevent scams and suspicious projects from raising funds through IEOs. Further, as exchanges act as mediators, projects can get significantly more exposure, interest, and credibility. After a successful IEO, the token issuers pay a listing fee to the exchange, along with a pre-determined amount of tokens for the use of the exchange’s platform services. IEOs gave birth to some of the most well-known blockchain projects of today including Polygon and Elrond. In Thailand, as of March 2022, there is no authorized digital asset exchange which is granted permission to conduct an IEO.

Initial Decentralized Exchange Offering (IDO):

While IEOs solved some of the problems which existed in the ICO market, proponents of dApps faced a dilemma, as the IEO process is a centralized process, relying on a centralized exchange such as Binance or FTX. Proponents of dApps claimed that decentralization could remove human fraud and error, speed up the process, and lower fundraising fees. Consequently, they needed to find an alternative to IEOs.

IDOs, which are a decentralized version of IEOs, originated in 2019 when Decentralized Exchanges (DEXs), a blockchain-based peer-to-peer exchange where transactions occur directly between crypto traders, gained popularity. IDOs use a DEX to facilitate the token sale via the DEX’s IDO launchpad. IDO launchpads are fully automated and run on blockchains using smart contracts. The most popular ones include BSC Pad, Polkastarter, DAO Maker, and Solanium. In order to raise funds, a fundraising project is submitted to an IDO launchpad. If the project meets the launchpad’s standards (as assessed by the community, the launchpad team, or the 3rd party auditor), the project owner(s) are permitted to issue their tokens on the DEX. These assessment processes usually cover only the project code and whitepaper, and do not require disclosing the identity of the project owner, making the process substantially less strict than the IEO process.

Image source: NGRAVE – The Crypto Funding Hype Cycle. From the first ICO in 2013 to the first IDO in 2019. Crypto funding models are continuously evolving to improve upon inherent pitfalls. Initially introduced by Ruben Merre in a 2019 article.

One of the most successful IDO fundraising cases conducted by a Thai dApp is GuildFi project. GuildFi is a Play-to-Earn (P2E) Game-Finance (GameFi) community where players, NFT owners, and game developers are connected. As GameFi requires a player to own NFTs to play games, GuildFi helps players who don’t own an NFT to borrow it from NFT owners. After a player earns income from the game, the income will be shared between players, NFT owners, and the platform. GuildFi also acts as a venture builder and invests in high potential GameFi projects before uploading the game to its platform community to bring traffic into the new game.

Apart from ICO, IEO, and IDO, where the majority of tokens raised are utility tokens, the fall of ICO also created another form of regulated fundraising method: Security Token Offering (STO). STO is an issuance of securities in the form of digital tokens on blockchain, backed by a real-world asset such as stocks, bonds, REITs, or commodities. Such digital tokens are called security tokens, and are a digital representation of the asset to the holder. Since security tokens need to be backed by real-world assets, they are deemed to be a security and are highly regulated by the SEC in many countries. The STO market is therefore relatively small and less liquid compared to ICO, IEO, and IDO markets. In Thailand, STO and security tokens are governed under a Securities and Exchange Act and regulators are in the process of developing the necessary infrastructure to support STO activity.

What Type of Fundraising Method is Suitable for Startups?

Blockchain startups and projects should perform token fundraising via private placement since the companies can gain instant funding and other benefits from investors without giving up ownership or voting rights. The token fundraising process is also substantially more efficient in terms of cost and time since the companies do not need to pay for investment bankers fee or spend time restructuring the organization and preparing tremendous documentation as required for the traditional IPO. The company or project owner can approach several angel investors or institutional investors to gain advantages such as increasing the project’s credibility, providing operational support, or helping the company grow its network and ultimately developing a concrete protocol. By taking these actions in the private placement stage, the company or project owner can later execute an IEO/IDO at a higher price compared to presale round, or raise funds via traditional debt or equity as needed. In general, it is still not recommended for dApp startups to execute an ICO, as ICOs are less credible and more costly compared to IEO/IDO. Low credibility and lack of investor awareness could prevent startups from raising sufficient funding. Thus, ICOs require the projects to pay a significantly large sum of marketing budget to build their trustworthiness and raise funding awareness, whereas IEO/IDO can utilize their own credibility and existing customer base nearly at no cost. Nevertheless, this is subject to each country’s regulations. For instance, in Thailand, as of March 2022, there is currently no digital asset exchange that is permitted by the SEC to perform an IEO and most of the tokens must be raised via authorized ICO Portal.

Further, startups should be wary of raising funds via both equity and token, since it may create a conflict of interest between equity holders and token holders. This conflict of interest occur since the causes of appreciation of equity and token are completely different. The appreciation of equity value is subject to generated cash flow and expected growth of the company. On the other side, the appreciation of token value is tied to the pure demand of the token. To illustrate, there might be a case where a token holder attempts to convince the company to spend unreasonably expensive investment just to increase the traffic and the demand of the token. Thus, to remove this conflict of interest, a dApp startup should either raise funds via token or equity. Otherwise, it needs to manage majority of the investors to hold equal amounts of tokens and equity.

What Type of Fundraising Method Is Suitable for Investors?

In general, dApp startups want funding from institutional investors, as these investors can offer a business instant credibility, operational support, and extended connections. This equips the institutional investor with high negotiating power. Thus, institutional investors who believe in the roadmap of a project and its team should invest in private placements in order to maximize financial return, as tokens are offered at a discount price. Retail investors are usually unable to access private rounds unless they have a good network with the project owner, but may still find upside in investing via IEOs or IDOs.

Token investments provide a crucial benefit to angels and institutional investors who invested in the private round: the ability to turn over cash flow. Unlike an equity investment, which requires an extensive holding period, token investments allow early-stage investors to exit at a significantly shorter investment horizon, since pushing a project through IEO and IDO, where these investors unload their token to realize their profit, is considerably easier and thus faster than traditional equity IPO. In addition, the token can be staked, during the holding period to gain more return along with, of course, risk. These benefits allow the investors to realize their profit quicker and manage their limited cash flow more flexibly.

Opportunities of Token Fundraising for Financial Institutions

Though equity and token fundraising will continue to co-exist in the future since the causes of capital appreciation are different, token fundraising may still heavily disrupt existing financial institutions’ services, particularly as a lender or underwriter. However, there is room for financial institutions to engage with the token fundraising process.

Loan Provider

In a similar fashion to how financial institutions provide lending to traditional small businesses, financial institutions can provide financing to registered dApp startups or individuals who want to create their dApp projects. Financial institutions have much financial and business expertise where most of the dApp projects are running their business. This could include business loans, project financing, or even sponsorship of activities such as gaming, in exchange for interest and/or other types of dApp incentives.

ICO Portal Provider

One of the major weaknesses of ICO and IDO is the lack of trustworthiness. Financial institutions have credibility in the eyes of consumers and could create their own ICO portal to act as a lead underwriter for any token fundraising projects. In addition, there is a growing trend where regulated firms wish to initiate project financing by raising funds via the token. For example, GDH 559, a leading film studio in Thailand, raised funds by selling utility tokens via Kubix, Kasikornbank’s affiliate which operates an ICO Portal, to fund the movie “Bpoop Phaeh Saniwaat 2”. The utility tokens not only provide monetary return to token holders, but also provide special privileges, such as the right to attend the movie premiere and the right to receive special souvenirs. Another use case is the issuance of investment tokens. For instance, in October 2021, Sansiri, one of the largest real estate developers in Thailand, raised 2400 million Thai Baht by selling Sirihub investment tokens backed by the cash flow generated by its real estate, providing up to 8 percent annual return to the token holders. Unlike security tokens, investment tokens do not provide ownership over the asset, but rather the right to receive the cash flow generated.

In accordance with the Emergency Decree on Digital Asset Businesses B.E. 2561, the Thai SEC currently only regulates raising funds via investment tokens and non-instant utility tokens (utility tokens which investors cannot use immediately), both of which must be raised via authorized ICO Portal only. However, it has not yet regulated fundraising via instant utility tokens (utility tokens which investors can use immediately). As of March 2022, the SEC is considering requiring any fundraisers who want to list instant utility tokens on exchanges to seek SEC approval or use an ICO portal. This potential regulation could create more traffic for ICO portal providers.

KYC Information Provider

When regulations mature, regulators may begin forcing registered dApp startups to KYC their users. Since financial institutions have extensive customer data and expertise, they can help dApps comply with AML regulations by acting as an information provider or consultant for startups to conduct KYC and onboard customers who want to use dApp service.

Investment

Lastly, financial institutions (FIs) can invest in and support dApp projects by purchasing tokens. dApp and blockchain protocols will contribute a considerable role in financial and other sectors in the future, and financial institutions can capture capital gains by investing in these technologies while they are still in their infancy stage. As providing funding to these startups allows them to kickstart their ideas, FI investments can help shape how this industry develops. In addition, financial institutions can impact the growth of these startups by providing operational support, expertise, insights, and connection to other institutional investors.

Token fundraising will be a large part of company funding and project financing in the future, and financial institutions should take the opportunity to gain knowledge and build up their capabilities in this industry now. This will enable them to better assess the next investment potential in the dApp industry. Perhaps, this could become an origin of a new business model where financial institutions could advise retail investors on investing in dApp startups, or provide tools to help investors evaluate proposed token fundraising deals. By doing so, financial institutions can utilize their credibility and provide other investors with a safer and easier way to invest.

What’s Next?

Token fundraising grants dApp projects, as well as traditional companies, a new source of capital; faster, cheaper, more flexible than ever before. IEOs and IDOs have emerged to mitigate many of the problems seen in the ICO market, and in the future, will co-exist as an alternative funding method alongside traditional fundraising. However, the traditional ICO method will continue to lose popularity and shift to a credibility-upgraded version, the ICO portal. Further, the development of the token fundraising market is not yet mature; new methods may continue to emerge and be further developed, including the use of NFTs for fundraising and the tokenization of real-world assets.

Author: Pobtawan Tachachatwanich (Pob)

Editor: Krongkamol Deleon (Joy), Warittha Chalanonniwat (Paeng)

Special shout-out: Wanwares Boonkong (Pin)

Sources:

- https://app.cbinsights.com/research/report/blockchain-tech-research-reports/

- https://www2.deloitte.com/content/dam/Deloitte/cn/Documents/audit/deloitte-cn-audit-security-token-offering-en-201009.pdf

- https://www.investopedia.com/terms/i/initial-coin-offering-ico.asp

- https://medium.com/@Athenablockchain/how-tokenized-private-placements-of-securities-and-the-development-of-markets-will-create-trading-a3603d30449c

- https://cryptonews.com/guides/what-is-an-initial-exchange-offering.htm

- https://www.gemini.com/cryptopedia/ieo-crypto-ido-crypto-initial-exchange-offering

- https://www.finyear.com/Tokenized-Venture-Capital_a41546.html

- https://newsletter.banklesshq.com/p/how-you-can-participate-in-defi-fundraising?utm_source=url

- https://www.nfx.com/post/token-investing/

- https://www.ingwb.com/binaries/content/assets/insights/themes/distributed-ledger-technology/defi_white_paper_v2.0.pdf

- https://www.sec.or.th/TH/Pages/News_Detail.aspx?SECID=8991&NewsNo=114&NewsYear=2564&Lang=TH

- https://www.sec.or.th/TH/Pages/News_Detail.aspx?SECID=9339

- https://www.sec.or.th/TH/Template3/Articles/2565/060165.pdf

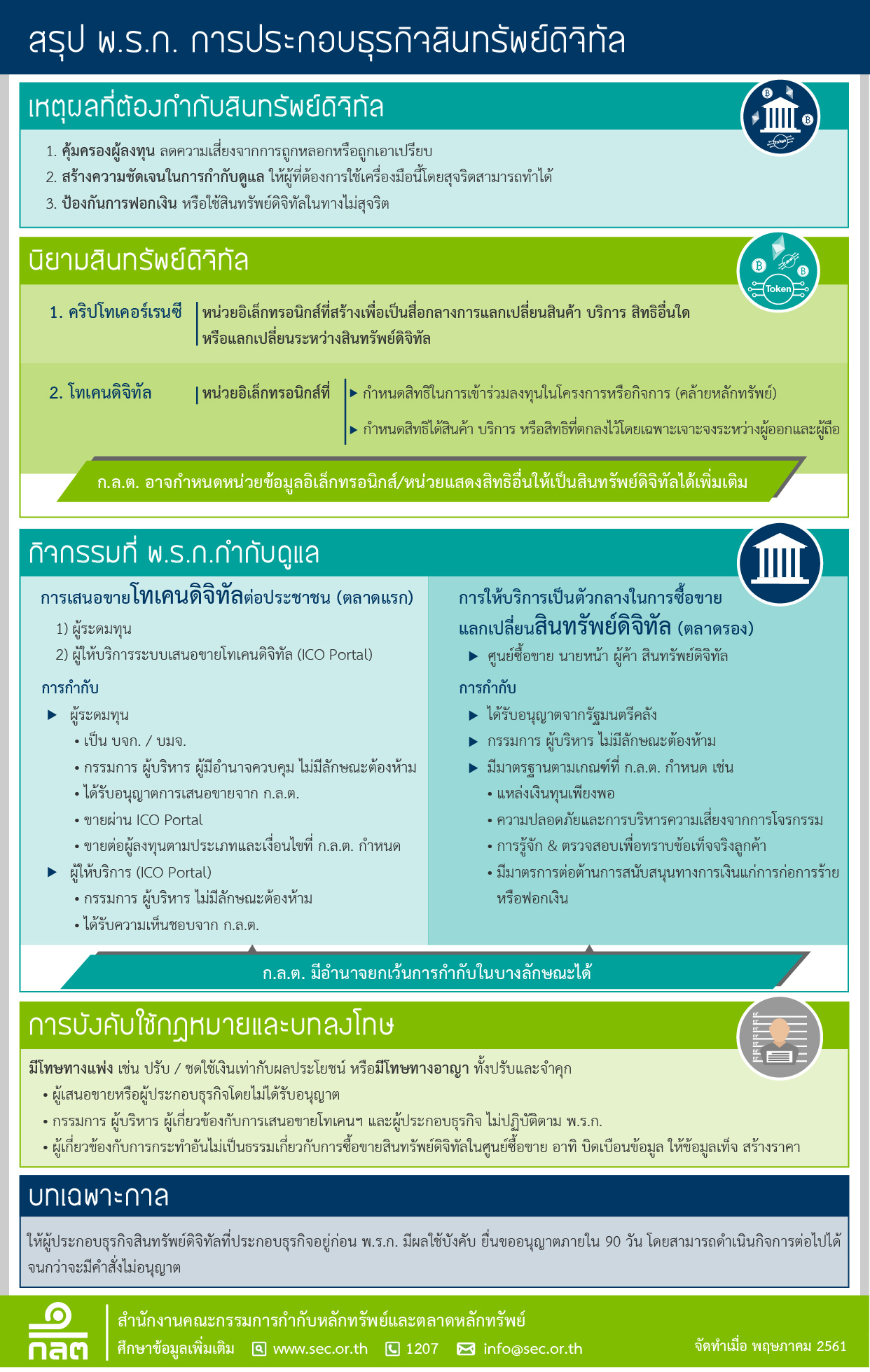

- https://www.sec.or.th/TH/PublishingImages/Pages/Shortcut/DigitalAsset/digitalasset_summary.jpg

{kind=link}