Introduction: From SaaS to AaaS — A Paradigm Shift in Finance

Introduction: From SaaS to AaaS — A Paradigm Shift in Finance

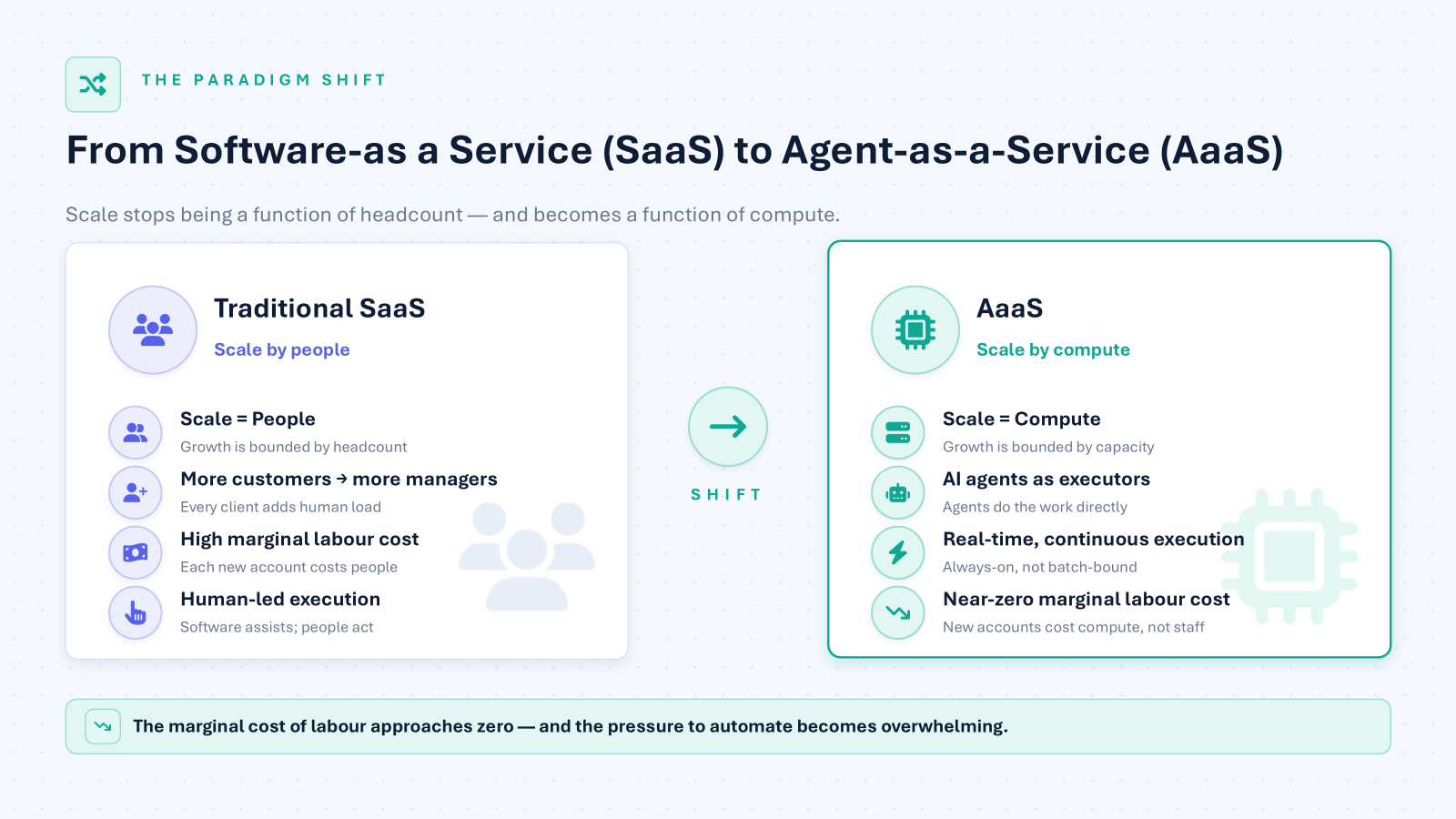

There is a quiet but profound reordering happening at the heart of financial services. For decades, the industry has operated on a simple assumption: scale requires people. More customers mean more relationship managers, more compliance officers, more operations staff. Technology — in the form of SaaS — made this human layer more efficient, but it never eliminated it.

That assumption is now being challenged by the transition from Software-as-a-Service (SaaS) to Agent-as-a-Service (AaaS), shifting the market from passive digital assistants toward Agentic AI—systems capable of operating as independent principal actors with full transactional autonomy. The clearest distillation of this evolution lies in enterprise fraud response. While a traditional SaaS model merely flags a suspicious transaction and pauses for human intervention, an AaaS model independently executes the entire detect-decide-resolve loop; it assesses the risk, freezes the compromised card, initiates an AI-driven voice call to confirm intent with the customer in their native language, and triggers backend systems to issue a secure digital replacement. By handling the end-to-end workflow autonomously, complex processes that once relied on a fragmented chain of back-office operations are resolved securely in seconds.

The economic implications are significant. In the traditional model, scaling a financial services operation means hiring. In the agentic model, scaling is constrained only by compute and API access. This is not an incremental improvement — it is the first time in history that the marginal cost of “labor” in financial services approaches zero. For the first time, an individual portfolio can be genuinely bespoke, a loan can be underwritten in real time, and a cross-border payment can be routed optimally in milliseconds — all without a human in the loop.

This article explores what that shift looks like across payments, lending, and wealth management; examines the infrastructure gaps that must be addressed; and identifies where Beacon VC believes the most defensible investment opportunities lie.

Deepening the Impact: Agentic AI Across Financial Services

The following use cases are structured by operational maturity — differentiating between immediate, near-term deployments and emerging, longer-horizon applications —across the three fintech pillars, Payments, Lending, and Wealth Management, where agentic AI is driving the most profound structural impact.

1. Payments: From Manual Checkouts to Autonomous Execution

Payments is where agentic AI found its first foothold. Transactions are discrete, measurable, and endlessly repetitive – the ideal conditions for autonomous execution.

Consumer-facing agents are crossing from recommendation to transactional autonomy. Tell it, “find this jacket cheaper and buy it”— and it navigates to the brand’s website and completes the purchase on the shopper’s behalf. Amazon’s Buy for Me already does this. This pattern is being extended to travel, retail, and subscription management.

On the enterprise side, autonomous fraud interdiction is turning fraud alert systems into defense engines. Commonwealth Bank of Australia (CBA) has deployed an advanced agentic AI system that monitors over 80 million daily interactions, autonomously scans payment metadata around the clock, evaluates threat severity in real time, and independently drafts, simulates, and proposes new transaction detection rules to intercept emerging scams at machine speed. Its technology reduces customer fraud losses by more than 20% in the first half of 2026.

Two frontier use cases are worth watching. The first is machine-to-machine payments, where agents can consume a service, pay another agent, and settle a transaction automatically. The second is agentic treasury management, which follows the same logic: instead of a periodic back-office task, AI continuously monitors multi-currency balances, liquidity, FX exposure, and macroeconomic indicators, then independently optimizes short-term yield strategies — turning treasury into an always-on optimization engine that acts the moment a gap appears.

2. Lending: From Static Snapshots to Continuous Intelligence

Lending has historically faced a structural data problem: credit decisions are forced to rely on a static financial snapshot frozen at the exact moment of application approval.

Agentic underwriting models are dissolving this operational constraint by continuously orchestrating the entire data ingestion and extraction process. TD Bank’s first agentic AI model is live across its mortgage applications. The autonomous agent ingests unstructured data from disparate client documents, dynamically calculates and verifies multi-source income, runs consent checks, and validates the entire package against strict risk policy guidelines while simultaneously hunting for application discrepancies. By executing this complex, data-heavy retrieval loop before a human reviews the file, the bank compressed its pre-adjudication summary timeline from a historical average of fifteen hours down to less than three minutes.

Looking ahead, continuous credit monitoring — agents keeping permanent watch over commercial portfolios, adjusting limits as cash flow shifts — will make annual covenant reviews feel obsolete. Agent-led underwriting research is close behind: systems that scour the open web for a corporate borrower’s market sentiment, ESG record and news exposure, flagging risk before it reaches the balance sheet.

More transformative still is the shift from reactive loan servicing to proactive intervention. Intelligent servicing agents monitor behavioral signals across a borrower’s accounts and reach out with a pre-approved, customized restructuring plan before a payment is missed — not after. This is not just operationally efficient; it is fundamentally better risk management.

3. Wealth Management: From Mass Customization to Individual Portfolios

Wealth management has long promised personalization but delivered segmentation: clients are grouped into risk buckets and assigned model portfolios. True personalization has remained too expensive to deliver at scale.

Agentic AI changes the unit economics. The shift is from a fixed ruleset applied to everyone to a daily-harvesting-and-rebalancing agent. Magnifi’s always-on agent monitors over $5 billion in client assets. When markets move overnight, it reprices the risk, identifies which losses are worth harvesting, and drafts a rebalancing plan tailored to that client’s specific holdings.

Further ahead lies the autonomous family office: an agent that coordinates across financial planning, estate management, tax optimization, and day-to-day bill payment, interfacing directly with a client’s lawyer and accountant agents. Behavioral coaching agents could add another layer, detecting emotional patterns in transaction histories (panic selling, impulsive spending) and intervening before a mistake becomes a loss.

The Missing Infrastructure: Gaps That Must Be Solved

The use cases above are compelling. But the infrastructure required to support them safely and at scale does not yet fully exist. This gap is, from an investor’s perspective, where the opportunity is most concentrated.

Identity and authorization for agents is perhaps the most acute problem. When an AI agent presents a corporate credit card at checkout, how does the merchant — or the bank — verify that the agent is genuinely authorized? The current answer is: it largely cannot. Solving this requires the development of verifiable credentials for agents: cryptographic attestations of an agent’s identity, scope of authority, and transaction history, analogous to the OAuth frameworks that govern human access to digital services. Alongside this, agentic behavioral scoring — dynamic risk assessment of agents based on their historical transaction patterns, dispute rates, and counterparty consistency — will be essential.

Policy orchestration and asset control presents an equally fundamental challenge. If an agent is authorized to manage a $10 million treasury position, what prevents it from breaching internal risk limits at 3am? Financial institutions need deterministic policy layers — programmable guardrails that constrain an agent’s actions within defined parameters, in real time. This is not a product that exists off the shelf today.

Developing new infrastructure is the critical bottleneck for the Agentic Economy, as legacy payment networks are fundamentally unsuited for machine velocity. Legacy rails like ACH and SWIFT were architected for human-initiated, batch-processed workflows, whereas autonomous agents require real-time, machine-to-machine clearinghouses that clear and settle in milliseconds. However, upgrading settlement speed is meaningless without addressing the interoperability gap; currently, specialized financial bots cannot transact with one another due to incompatible data schemas. This infrastructure friction is further compounded by fragmented data quality and restricted data access. If the underlying financial data fed into an agentic pipeline is non-standardized or dirty, the transaction will fail automatically, regardless of backend clearing speeds. Building this new infrastructure layer—specifically via programmable blockchain-based rails and stablecoin liquidity pools—is therefore a functional institutional necessity to provide a unified, instant settlement fabric for autonomous commerce.

Finally, liability and audit in an agentic system represents a genuinely novel legal and compliance challenge. When an autonomous agent makes a losing trade or a mis-sold insurance recommendation, the forensic trail needed to assign liability and demonstrate regulatory compliance does not yet exist in standard form. Building that audit infrastructure is a prerequisite for banks to deploy agents in regulated contexts.

The Enabling Technologies: Blockchain and Quantum Security

Two complementary technologies are emerging as essential plumbing for a secure agentic financial system, serving as critical infrastructure layers that solve the machine trust problem across different time horizons.

In the near term, Blockchain serves as the immediate Trust and Audit Layer, providing a practical operational blueprint for non-human entities. By giving agents cryptographic identities through secure smart wallets and recording their independent actions on an immutable ledger, blockchain delivers the regulatory-grade accountability and permanent forensic trails that compliance officers will mandate before allowing autonomous capital deployment at scale.

Over a longer horizon, Quantum Security emerges as the ultimate Integrity Layer to protect cryptographic keys and sensitive financial data from quantum-enabled attacks. Because future quantum computers will possess the capability to compromise legacy encryption keys, transitioning to post-quantum cryptographic standards becomes a necessary insurance policy to secure machine identities and long-term asset transfers. This structural defense is further reinforced by advanced privacy tools like Zero-Knowledge Proofs (ZKPs) and Fully Homomorphic Encryption (FHE), which enable agents to verify creditworthiness, identity, or compliance without exposing the underlying sensitive data.

Investment Thesis: Where Beacon VC Is Focusing

The shift is not a forecast — adoption, capital, and talent are already moving toward these infrastructure layers. Mastercard launched Agent Pay in April 2025 and has already completed live authenticated agentic transactions across multiple markets. Venture investment in agentic AI reached $6.42 billion, and banks are reallocating talent accordingly, with Lloyds hiring 300 AI specialists into a 1,000-strong AI team.

From this analysis, we see four high-conviction investment areas:

1. Real-Time Liquidity and Programmable Rails. The move from messaging-based banking (SWIFT) to value-based banking (blockchain) is not a speculative bet — it is a functional requirement for the agentic economy. Assets are already migrating: BlackRock’s BUIDL tokenized Treasury fund holds roughly $2.3 billion, while cross-border B2B stablecoin payments are projected to reach $5 trillion by 2035, and tokenized assets overall could reach $16 trillion by 2030 — around 10% of global GDP. Startups bridging legacy core banking systems to tokenized liquidity pools and B2B stablecoin infrastructure occupy a structurally defensible position.

2. Agentic Security and Verification. AI is probabilistic by nature; the financial system requires deterministic outcomes. AI-cybersecurity is scaling: by 2030 the agentic AI-security segment is expected to reach $7.84 billion and post-quantum cryptography $2.84 billion. Cost is seen as the main driver, as global fraud and scam losses hit $579.4 billion in 2025, with every $1 lost costing around $5 to recover. The most valuable companies in this space will build “checker” layers that mathematically verify an agent’s intended action is safe before the bank’s ledger is touched. Verification oracles, formal verification for AI logic, and post-quantum cryptography infrastructure are all in scope.

3. The “Agentic RegTech” Stack. Before any regulated financial institution can deploy an autonomous agent, it must demonstrate to regulators that the agent has a verifiable identity, a defined scope of authority, and a compliance-grade audit trail. The pain is quantified and rising: banks in the US and Canada spend $61 billion annually on financial crime compliance, with 99% reporting rising costs. AI-in-RegTech is projected to grow from $2.57 billion in 2025 to $12.33 billion by 2030. Companies building attestation engines, dynamic KYC for AI systems, and privacy-preserving data compliance tools sit directly in the critical path of institutional agentic deployment.

4. Autonomous FinOps Middleware. The large incumbent banks are sitting on decades of fragmented, legacy infrastructure. Full core replacement is slow and expensive: CBA’s core replacement took five years and cost US$750 million. This creates a large middleware opportunity, with the AI-orchestration market projected to reach $30.2 billion by 2030 and the legacy-bridging market forecast to reach $13.34 billion. The startup that can act as “connective tissue” between a modern LLM and a bank’s COBOL-era core system — enabling agent orchestration without a full infrastructure rebuild — will find a captive market and very high switching costs. Agent-to-legacy adapters and cross-institution collaboration protocols are unsexy but highly defensible plays in this space.

Conclusion: Toward a Glass-Box Finance System

The future of the financial landscape hinges on transitioning to a “Glass-Box Finance” paradigm. This architecture shifts away from opaque, un-auditable “black-box” systems, replacing them with absolute transparency, real-time auditability, and deterministic explainability at every layer of machine execution. Regulators, institutions, and consumers can peer directly into the “glass box” to verify the exact reasoning behind an agentic transaction or risk decision the millisecond it occurs.

The transition will not be without friction. The infrastructure gaps, data silos, and nascent regulatory frameworks are complex hurdles. However, the economic logic remains irreversible: as the marginal cost of machine labor approaches zero, competitive pressure to automate will become overwhelming.

The future of finance is not merely automated; it is autonomous, transparent, and quantum-secure. The founders building toward that future are not writing features — they are writing the foundational operating system for an economy where the bank itself functions as an intelligent, self-proving protocol. At Beacon VC, we believe the category-defining fintechs of the next decade are being built right now—forging the compliance stacks and infrastructure layers necessary to make the Agentic Economy safe enough to trust.

Authors: Wanwares Boonkong (Pin), Thapanawit (Ping) Janthra

Editor: Woraphot (Ping) Kingkawkantong

References:

CommBank develops AI agent that spots new fraud and helps build defences — Commonwealth Ban

TD Launches Agentic AI to Transform Real Estate Secured Lending from End to End — TD Bank Newsroom

15 Hours to Three Minutes: TD’s Agentic AI Launch and the New Underwriting Clock — Fundmore.ai

Artificial Intelligence (AI) for Debt Collection in 2026 — ScienceSoft

From Reactive to Proactive: How Agentic AI is Rewiring Wealth Management — Magnifi

The Agentic Funding Shift: $6.42B in 2025, Fewer But Bigger Bets in 2026 — AgentMarketCap

Agentic AI Startup Funding 2025–2026 — New Market Pitch

Stablecoins in payments: What the raw transaction numbers miss — McKinsey & Company

Artificial Intelligence — Lloyds Banking Group

Lloyds Banking Group to hire 300 tech experts to work on AI — The Guardian

Biostimulants Market Report, 2025–2030 — MarketsandMarkets

Stablecoin Cross-border B2B Transactions to Surpass $5tn — Juniper Research

Asset Tokenization: A $16 Trillion Opportunity by 2030 — BCG & ADDX

Post-quantum Cryptography (PQC) Market Report, 2025–2030 — MarketsandMarkets

2026 Global Financial Crime Report — Nasdaq Verafin

Artificial Intelligence in RegTech Global Market Report — The Business Research Company

Banking on AI: Banking Top 10 Trends for 2024 — Accenture

AI Orchestration Market Report, 2025–2030 — MarketsandMarkets

Mainframe Modernization Market Report, 2025–2030 — MarketsandMarkets