Artificial intelligence is rapidly evolving, moving beyond simple automation to create truly intelligent systems capable of independent action.This evolution has led to the emergence of the AI agent, a sophisticated form of AI designed to perceive its environment, make decisions, and act autonomously to achieve specific goals with minimal human intervention. This article explores the journey of AI from rule-based automation to the dawn of agentic AI, examining its evolution, distinguishing characteristics, operational mechanisms, diverse applications, and the challenges and opportunities that lie ahead in its widespread adoption.

What is AI Agent and how has agentic AI evolved?

Agentic AI or AI agent refers to AI applications designed to function and make decisions to reach specific goals, under changing environments, autonomously with minimal human intervention. To gain a deeper understanding of Agentic AI, it is essential to explore its evolution, its differences from other AI applications, how it works, and its diverse use cases.

Although there are some controversies around whether the terms “Agentic AI” and “AI agent” can be used interchangeably[1], for the purpose of this article, “Agentic AI” is considered analogous to the brain whereas AI agents are seen as the hands-taking action as the brain commands.

Agentic AI evolution and differences from other AI applications

The evolution of Agentic AI can be traced back to early robotic process automation (RPA), which relied on predefined rules and workflows. These systems excelled in environments with clear parameters and predictable conditions, performing structured and repetitive tasks efficiently. However, advancements in large language models (LLMs) have significantly expanded the capabilities of AI systems, resulting in the introduction of conversational AI. Conversational AI is capable of understanding and responding to human languages. Early conversational AI systems, such as chatbots, provided scripted responses within predefined domains.

The integration of Conversational AI with RPA gave rise to AI copilots that could think and act beyond predefined rules. These AI copilots understand natural language, adapt to dynamic environments, and perform more complex tasks. They offer contextual assistance and support human decision-making. While they enhance productivity by interpreting complex inputs and providing intelligent suggestions, they ultimately rely on human direction to guide their actions. As AI models become more sophisticated, automation evolves to handle more complexity and achieve greater autonomy. This progression will culminate in the emergence of Agentic AI—fully autonomous systems capable of tackling sophisticated tasks with minimal human oversight. Currently, various use cases illustrate an intermediate stage between AI copilots and fully autonomous AI agents, where AI systems exhibit greater independence while still requiring some human intervention.

Note: While both RPA and AI agents are well-suited for high-volume, repetitive tasks, RPA is generally limited to tasks with predictable, single outcomes triggered by specific conditions. AI agents, on the other hand, can handle tasks with multiple potential outcomes, adapting and adjusting their approach based on the current situation.

How it works

To better illustrate how Agentic AI could be applied to real-life workflows, take loan assessment as an example. In a normal day, when a relationship manager (RM) receives a loan application from a borrower, they gather data such as financial statements, commercial agreements, and credit bureau data from multiple sources. The RM then collaborates with credit analysts to analyze this data, create a credit approval memo, and seek approval from an authorized person. This process can take up to three weeks or longer.

With agentic AI, the RM’s role would shift from data collection, collaboration with credit analysts, and seeking approvals to simply providing prompts to the AI. The agentic AI would function as a virtual employee, handling all the tasks and reporting the final result back to the RM. This result could be an email to the borrower rejecting the loan or a confirmation email approving the loan with next-step instructions.

To reach a decision, the AI agent would break down the process into subtasks, assigning them to specialized AI agents. For example, an AI data collection agent would gather information from various sources independently, an AI analyst agent would assess creditworthiness and repayment capabilities, and an AI memo agent would compile the analysis and create a credit memo for review by the RM and analysts.

The agentic AI would transparently demonstrate its decision-making process for validation by the RM. If the RM trusts the AI’s reasoning, the RM can authorize the AI to proceed. Thus, the RM’s role evolves from performing all tasks to becoming a validator. This human validation is crucial during the AI’s development phase. However, as the AI’s reliability increases, the RM may eventually only need to oversee the process, allowing the AI to proceed without intervention.

Benefits of Agentic AI

AI agents are rapidly transforming the way businesses operate and interact with their customers. By automating processes, enhancing decision-making, and personalizing experiences, these intelligent systems are driving significant improvements across various sectors. The following sections explore key benefits of AI agent implementation, showcasing real-world examples of how these technologies are boosting efficiency and productivity, accelerating and enhancing decision-making, and ultimately, improving customer experience.

-

- Boosting Efficiency and Productivity

AI agents can significantly boost efficiency and productivity by streamlining business processes and automating unstructured tasks. For example, in customer service, AI agents can resolve customer issues by understanding their pain points, gathering relevant information from databases (including historical data), and taking appropriate action. By swiftly completing tasks that typically consume significant human resources, AI agents free up staff to focus on more strategic and meaningful work, ultimately leading to improved overall productivity. Agentic AI goes beyond the capabilities of AI copilots. While Agentic AI can make autonomous decisions and take appropriate actions, AI copilots function alongside humans, assisting but not independently deciding or acting.

Real-world use cases

-

-

-

- Amazon’s agentic AI (“Amazon’s Warehouse Robots”), manages inventory, predicts demand, and optimizes delivery routes in real-time. These robots navigate complex warehouse environments, adapt to changing conditions, and autonomously transport goods. By leveraging agentic AI, Amazon not only replaces human workers with robots capable of precise task execution, freeing up staff for more valuable work, but also reduces costs associated with scaling its business and hiring additional personnel.[2]

- PepsiCo leverages agentic AI to streamline recruitment by matching candidates to job roles. The AI scans profiles across multiple sources to generate tailored candidate lists for each position. This enhances productivity, allowing HR teams to focus on higher-value tasks.[3]

-

- Accelerating and Enhancing Decision-Making

-

AI agents excel at enhancing decision-making by quickly and accurately analyzing large volumes of data. They can provide rapid analysis of complex scenarios, accelerating the decision-making process. This is particularly valuable in time-sensitive situations where quick action is crucial. They can also simulate different scenarios and predict potential outcomes, allowing decision-makers to evaluate options quickly.

Real-world use case

-

-

-

- Darktrace’s Enterprise Immune System leverages AI to learn an organization’s typical network behavior. Upon detecting anomalous activity, such as unusual logins or data transfers, the system autonomously blocks threats or isolates compromised devices, effectively halting attacks before they can spread. Relying on manual human review for such tasks is inherently slower and more prone to error, preventing the real-time action needed to minimize potential losses.

-

-

-

- Improving Customer Experience

AI agents can process vast amounts of data to deliver personalized recommendations based on each customer’s historical data, thereby improving satisfaction and loyalty. Previously, businesses struggled to customize recommendations for individual clients due to high costs, limited data, and time constraints. However, with AI agents, businesses can gain deep insights into customer preferences and provide tailored products or services in real-time. This capability enhances the overall customer experience and strengthens customer relationships. As AI agents achieve greater reliability and earn user trust, they will become a valuable virtual workforce for supporting customers.

Real-world use case

-

-

-

- A digital health company, Livongo, has integrated Agentic AI into its diabetes management system. The AI autonomously analyzes continuous glucose monitoring (CGM) data, dietary habits, and physical activity metrics to generate personalized recommendations and actionable alerts. Instead of merely presenting data, it advises users on actions like consuming carbohydrates when glucose levels trend toward hypoglycemia. This not only saves cost and time for patients who would otherwise need frequent hospital visits and endure long queues but also improves their quality of life by providing real-time recommendations and enabling immediate action, resulting in a better customer experience. [4]

- A leading Dutch insurer has integrated AI agents into its claims management system, reducing processing time by 46% and increasing customer satisfaction by 9%. Upon receiving a claim, the AI analyzes eligibility for automated processing using predefined rules to assess coverage, liability, and other factors. It then takes appropriate actions, such as approving straightforward claims, rejecting those without coverage, or flagging complex cases for human review. [5]

-

-

Where AI Agents Will Be Adopted First

Due to several limitations hindering the widespread adoption of AI agents, only a few organizations are currently ready to embrace this technology. Enterprises are hesitant to integrate AI agents into their core operations, where unreliable decisions and actions could have detrimental consequences. Based on the capabilities and limitations of AI agents, their adoption is likely to follow these trends:

-

- Tasks or businesses associated with low-risk impact from decision-making will adopt AI Agent quickly

Due to the early stage of AI agents, enterprises are cautiously adopting them in low-risk decision-making areas. Current real-world applications reflect this trend, focusing on controllable risk environments. E-commerce companies, for example, are leveraging AI agents for customer support and personalized recommendations, where the impact of decisions is less severe. However, for high-impact decision areas, human oversight remains crucial.Enterprises must carefully consider the implications of maintaining a human presence in these processes.

-

- High data volume industries with robust data infrastructure will adopt AI agents more readily

Industries and organizations with robust digital data infrastructure and high data volumes are poised for faster AI agent adoption. These entities, like healthcare with its vast research data or customer service with its high volume of client interactions, already possess the digital foundation necessary for seamless AI integration. AI agents excel at processing and analyzing large datasets with speed and accuracy, surpassing human capabilities, making them invaluable in these data-rich environments. This advantage explains why tech companies and established enterprises, which typically manage data digitally, lead the way in AI agent adoption, while organizations relying on traditional, on-premise data storage may face a steeper learning curve.

-

- Early AI Agent Adoption Will Occur Horizontally Before Vertically

AI agents are expected to be adopted across industries for broad, non-specialized tasks—such as customer service and productivity enhancement—before they gain traction in industry-specific applications. In healthcare, for example, AI agents could be used for scheduling, payment processing, and insurance claims, but they are not yet reliable for technical tasks requiring medical expertise. Similarly, legal firms may leverage AI agents for regulatory research or document summarization, but AI is not yet advanced enough to provide legal opinions.

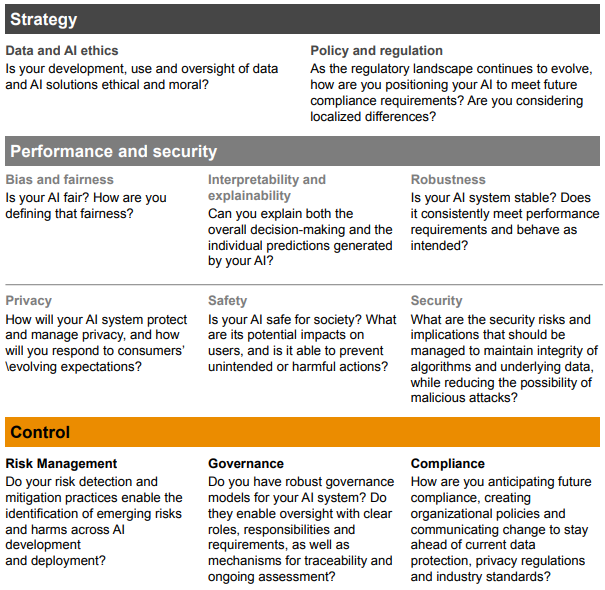

Challenges Preventing Wide Adoption of Agentic AI

Despite Agentic AI seeming to provide promising benefits to enterprises, AI agents have not yet been adopted widely. Most current applications of AI agents focus on straightforward, low-risk impact tasks such as solving customer issues, automating document reviews, or sending emails and scheduling calls. The use cases of AI agents on more complex tasks have not been widely seen yet. Most of the ideal use cases described previously are in the experimental stage and rely heavily on human oversight, reducing the value of using an AI agent.

For AI agents to gain widespread adoption among enterprises for complex and high-stakes tasks, several challenges must be addressed. The key barriers preventing widespread adoption of AI agents include:

-

- Lack of Trust in AI Agents Among Enterprises

A major obstacle to adoption is enterprises’ lack of confidence in AI agents. Organizations need transparency in how AI agents make decisions, process data, and ensure reliability. Startups developing AI agents must provide detailed documentation explaining how their models function and offer clear, understandable breakdowns for both technical and non-technical stakeholders. Additionally, security and compliance concerns are paramount. Enterprises need assurances that their data remains secure, and without strong security tools and frameworks, businesses will be hesitant to adopt AI agents.

-

- Data Privacy and Security Concerns

Data privacy and security are paramount concerns for enterprises considering the adoption of agentic AI. As AI agents access vast amounts of sensitive data such as financial records and medical histories, these systems’ reliance on extensive data necessitates careful management of its acquisition, storage, use, and disclosure, along with strict adherence to relevant regulations and industry standards like SOC 2 Type I/II, ISO 27001, HIPAA, and GDPR.

-

- High Upfront Costs and Integration Complexity

The high initial costs and complexity of integration remain significant hurdles. Data collection and training have yet to reach economies of scale that would drive costs down. Additionally, integrating AI agents into existing workflows requires extensive effort. For example, traditional hospitals looking to implement AI agents must migrate patient data from on-premise storage to cloud systems, establish policies for managing sensitive data access, and train staff to work effectively with AI technology.

Addressing these challenges is crucial for AI agents to gain widespread adoption across industries. As data privacy and security measurements are in place, trust issues are mitigated,and costs decrease, AI agents will become an integral part of enterprise workflow

The Emerging Business Opportunities in AI Agent Adoption

The challenges around AI agent adoption create business opportunities. As AI agents become more sophisticated and integrated into enterprises, various enabling technologies and services will be critical to accelerating their deployment. Startups and investors should monitor these key business opportunities closely, as these tools will play a pivotal role in facilitating AI agent adoption.

-

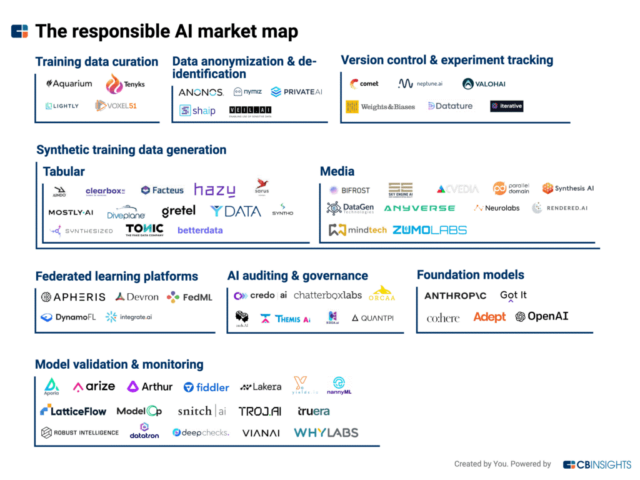

- Model validation and monitoring tools that help increase trust and reliability

For enterprises to trust and effectively use AI agents, they must fully understand how AI systems make decisions rather than relying on them blindly. Startups in this space are developing software that functions as a quality control system for AI, enabling companies to monitor their AI models in real-time. These platforms provide transparency by explaining why AI makes specific decisions, reducing the “black box” effect and helping businesses enhance AI accuracy and reliability. Enterprises can view these platforms as dashboards that offer visibility into AI decision-making, ensuring fairness, accountability, and compliance with industry regulations.

-

- Data privacy and security tools to ensure AI privacy and security[6]

To address data privacy and security concerns, enterprises should establish a comprehensive data governance framework. However, policies alone are insufficient; effective implementation requires the right tools. The following tools can help organizations manage data privacy and maintain compliance with relevant regulations and industry standards.

-

-

-

- Data masking and anonymization tools: Tools in this space help remove identity information from the data before using such data in AI models, mitigating the risks of unauthorized access and data breach.

- Access control and audit tools: Tools in this group help manage data access control, allowing only authorized users to access data. Additionally, they could track data access, detect, and address unauthorized access to users. Once enterprises set up a data policy framework, they can deploy such frameworks by using these tools.

- Data lineage and audit trail tools: These tools track the origin and movement of data, enabling users to understand its source, transformations, and ultimate destination. This creates an audit trail that demonstrates regulatory compliance.

-

-

-

- AI Agent enablers that help bring the cost down and address integration complexity

Several key technological advancements are emerging to address the cost and complexity barriers associated with AI agent development and deployment. Among these are decentralized GPU cloud services and robust metadata management solutions.

-

-

-

- Decentralized GPU Cloud Services

-

-

Training large language models and deploying AI agents in real-world applications requires significant GPU processing power, leading to high infrastructure costs. Decentralized GPU cloud services offer a solution by making computational resources more accessible and affordable. This model operates similarly to “Uber for the GPU world,” connecting users with idle GPU capacity to those who need affordable, scalable computing power. As AI agents continue to grow, decentralized GPU cloud services will likely gain traction, reducing dependency on traditional cloud providers and lowering entry barriers for AI startups.

-

-

-

- Metadata Management

-

-

Metadata management is a foundational requirement for AI agents to function effectively and scale within organizations. It helps AI agents interpret context, maintain structured knowledge, and make informed decisions while facilitating agent communication, task orchestration, and knowledge sharing across distributed systems. Essential features of metadata management tools include data cleaning, classification, and organization to ensure accuracy, integrity, and consistency. This market is currently dominated by major tech players such as Databricks, Snowflake, and IBM, which provide robust solutions for enterprises looking to manage metadata at scale.

Conclusion

As AI agents continue to advance, the transition from their current capabilities to fully autonomous systems will take time. However, their potential to transform industries is increasingly evident. By boosting productivity, enhancing decision-making, streamlining workflows, and improving customer experience, AI agents are poised to play a pivotal role in the future of automation. Despite this promise, widespread adoption still faces significant challenges, including cognitive architecture development, enterprise trust, infrastructure readiness, and integration complexity. Nevertheless, businesses that rely on structured processes and large datasets are likely to be early adopters, paving the way for broader industry acceptance. As enabling technologies mature and organizations gain confidence in AI-driven decision-making, AI agents will gradually become an integral part of enterprise operations. The future of AI agents extends beyond mere automation—it lies in the development of intelligent, adaptive systems that work seamlessly alongside humans, unlocking new opportunities for innovation and efficiency across industries.

Author: Warittha Chalanonniwat (Paeng)

Editors: Krongkamol deLeon (Joy), Woraphot Kingkawkantong (Ping)

Reference

- https://medium.com/towards-data-science/ai-assistants-copilots-and-agents-in-data-analytics-whats-the-difference-2e63f8fb2384

- https://www.linkedin.com/pulse/when-choose-ai-co-pilot-vs-agentic-lata-tewari-r2mqc/

- https://beam.ai/agents

- https://www.miquido.com/blog/ai-agents-use-cases/

- https://bytebridge.medium.com/ai-agents-current-status-industry-impact-and-job-market-implications-f8f1ccd0e01f

- https://www.automaited.com/resources/blog/6-types-of-processes-that-are-suitable-for-rpa

- https://www.linkedin.com/pulse/when-choose-ai-co-pilot-vs-agentic-lata-tewari-r2mqc/

- https://medium.com/towards-data-science/ai-assistants-copilots-and-agents-in-data-analytics-whats-the-difference-2e63f8fb2384

- https://medium.com/@elisowski/ai-agents-agentic-ai-and-autonomous-ai-are-they-the-same-2ca7fbf5474a

- https://www.linkedin.com/pulse/agentic-ai-cybersecurity-autonomous-adaptive-proactive-protection-ucpqe/

- https://medium.com/@elisowski/ai-agents-vs-agentic-ai-whats-the-difference-and-why-does-it-matter-03159ee8c2b4

- https://www.teqfocus.com/blog/top-5-benefits-of-agentic-ai-driven-workflows-in-the-pharma-and-healthcare-industries

- https://botpress.com/blog/real-world-applications-of-ai-agents#:~:text=Virtual%20Assistants,personalized%20and%20effective%20over%20time.

- https://www.endava.com/glossary/agentic-ai#:~:text=Agentic%20AI%20evolved%20from%20conversational,language%20and%20autonomously%20make%20decisions.

- https://www.digitalocean.com/resources/articles/agentic-ai

- https://medium.com/spheronfdn/5-leading-decentralized-computing-platforms-transforming-access-to-gpu-computational-power-d9673fe4e40a

- https://www.madrona.com/the-rise-of-ai-agent-infrastructure/

- https://www.forbes.com/sites/robtoews/2024/07/09/agents-are-the-future-of-ai-where-are-the-startup-opportunities/

- https://www.grandviewresearch.com/industry-analysis/metadata-management-tools-market-report

- https://www.ibm.com/think/topics/explainable-ai#:~:text=Explainable%20AI%20is%20used%20to,putting%20AI%20models%20into%20production.

- https://www.nvp.com/blog/ai-agents-enterprise-bridging-gap-agentic-ai/

- https://www.forumvc.com/2024-the-rise-of-agentic-ai-in-the-enterprise

- https://medium.com/@mparekh/ai-long-road-ahead-for-ai-agents-for-enterprises-and-consumers-rtz-494-c86861de6c1d

- https://www.ankursnewsletter.com/p/horizontal-ai-agents-vs-vertical

- https://medium.com/@HitachiVentures/the-dawn-of-agentic-ai-transforming-enterprise-automation-and-the-future-of-work-e30844d41f1e

- https://www.linkedin.com/pulse/agentic-ai-here-its-shaking-up-business-landscape-tiarne-hawkins-yonff/

- https://www.cbinsights.com/reports/CB-Insights_Future-Workforce-AI-Agents.pdf

- https://www.everestgrp.com/automation/navigating-the-agentic-ai-tech-landscape-discovering-the-ideal-strategic-partner-the-rising-enterprise-adoption-of-agentic-ai-blog.html

- https://cloud.google.com/transform/101-real-world-generative-ai-use-cases-from-industry-leaders

- https://www2.deloitte.com/us/en/insights/industry/technology/technology-media-and-telecom-predictions/2025/autonomous-generative-ai-agents-still-under-development.html

- https://www.leewayhertz.com/ai-loan-underwriting/#loan-underwriting-processes-with-generative-AI

- https://blog.langchain.dev/what-is-an-agent/

- https://www.kenresearch.com/industry-reports/global-ai-agent-market

- https://www.sequoiacap.com/podcast/training-data-harrison-chase/?itm_medium=related-content&itm_source=sequoiacap.com#are-agents-the-next-big-thing

- https://www.pwc.com/m1/en/publications/documents/2024/agentic-ai-the-new-frontier-in-genai-an-executive-playbook.pdf

- https://www.ft.com/content/36785ec8-6f9f-455f-ac74-645bcaa9e221

- https://www.finextra.com/blogposting/27196/agentic-ai-the-competitive-edge-finance-and-insurance-companies-need-to-stay-ahead

[1] https://medium.com/@elisowski/ai-agents-agentic-ai-and-autonomous-ai-are-they-the-same-2ca7fbf5474a

[2] https://medium.com/@elisowski/ai-agents-vs-agentic-ai-whats-the-difference-and-why-does-it-matter-03159ee8c2b4

[3] https://davoy.tech/agentic-ai-capabilities-and-applications/

[4] https://www.linkedin.com/pulse/agentic-ai-healthcare-real-world-use-cases-revolutionizing-hgobe

[5] https://beam.ai/resources/case-studies/dutch-insurance-claims-processing

[6][6] https://www.zartis.com/ai-and-data-protection/how-to-protect-your-ip-while-using-ai/

Image generated by Gemini

Image generated by Gemini